Topics:

Never Miss a Beat - Get Updates Direct to Your Inbox

FILTER:

How To Successfully Transition Staff When Buying a New Business

By Quiet Light

Having physical staff is often seen as a black mark against transferability. Some companies rely on the skills and personalities of their staff which introduces an element of risk into the transition of ownership. After all, there is no way to know exactly how staff will react to you.

Will their personality work with yours? Are they so loyal to the previous owner that they don’t want to work for someone new? Or, were they dissatisfied with their role before and see this as a perfect opportunity to move their career in a different direction?

Whether it is a personality clash with the new owner or the staff’s unhappiness at the intended future direction of the business, having staff sets up the potential for issues during a transition period.

However, as Bryan recently pointed out, staff can also make a transition significantly easier. A business with staff is generally less dependent on the owner which reduces your learning curve and gives you much more time to get familiar with the intricacies of the business.

Having staff acts as an amplifier during a transition: they can either make it much easier or much more difficult.

So how should you, as a buyer, address the situation of transitioning staff? When should you talk to them, and how can you get them to stick around during a transition?

https://www.youtube.com/watch?v=IZ2oxJIMt-c

First, Make Your Seller Comfortable by Saving Staff Discussions for the End of Due Diligence

Different sellers approach the issue of notifying their staff of the transition in different ways. Some like to tell their staff as early as possible. Others wait until they are absolutely certain the business is going to sell so they can relate firm plans to their employees and reduce their questions and concerns.

Regardless of what the seller chose in your transaction, you should plan to have discussions with staff towards the end of your due diligence. Tackle the less sensitive items first such as reviewing tax returns or bank statements.

Hopefully, the reasons for this are obvious. It would not make much sense to talk to staff before you have verified a seller’s financial records. If the financials cannot be verified, then the deal will not happen and there is no need to speak with the seller’s staff.

Although you may want to speak with staff early on in your due diligence – especially if the business depends on a few key employees – keep in mind that until the business closes, the seller is still responsible for its day to day operations. They won’t be eager to disrupt operations before a transition gets in motion.

When You Do Speak with Staff, Aim for Commitments Throughout the Transition

For a key employee, an acquisition will likely raise a lot of questions and a lot of uncertainties. You may have similar questions and uncertainties. So while it may initially seem like a great idea to have certain staff members stick around for years to come, you (or they) may not feel the same way 3-6 months after the acquisition.

Because of this, try to build in commitments that cover your transition period. Target bonuses, incentives, and most goals around a successful transition. This will give both you and the staff an opportunity to discover each other, the roles within the company, whether they are still a good fit, and whether they want to continue with the company.

You can always make new commitments after the transition for a longer-term arrangement. But, initially, your primary concern should be getting to a point where you can confidently fill any position needed.

3 Tips To Remember When Speaking To Staff

Set Expectations So The Staff Know What Is Coming

While many experts claim that an employee’s most common reaction to an acquisition is fear, I would argue that it is actually uncertainty (which eventually leads to fear).

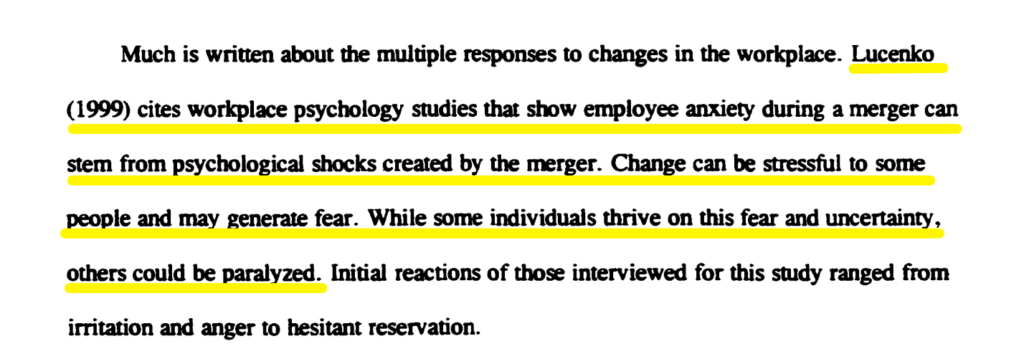

This uncertainty has a wide range of potential psychological effects on employees. In fact, a lot of research dollars is spent by large corporations who need to plan massively complex mergers and acquisitions.

In 1992, a physician by the name of Dr. Marks labeled the effects of a merger on employees as “merger syndrome”. And in 1992, Kristina Lucenko penned a psychological study that concluded the shock from learning of a merger creates employee anxiety, fear, and uncertainty. For some, this could be paralyzing.

While these studies were designed for large corporate mergers, the principles hold true for smaller acquisitions as well.

Since the #1 driver of negative employee reactions is a sense of uncertainty, you need to assure employees by setting their expectations and giving them some certainty.

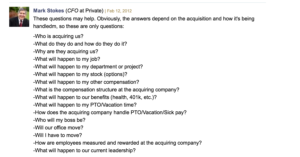

You can do this by understanding the basic questions employees have during an acquisition (there is a good discussion on Proformative on this very topic). But don’t just rely on the literature that’s been written on this topic. Take the time to ask the employees if they have any concerns or questions. Ask them what is most important to them during the transition, and how they would like to see things play out.

Ask The Staff To Document Job Procedures

If the seller does not already have a set of standard operating procedures in place, you should let the staff know that you’ll want them to document what they do on a day-to-day basis once you take over the company.

Having their processes documented will give you two things:

- You’ll get access to much more information about the business on a very detailed level

- If any employee decides to leave before the transition is finished, you’ll be able to fill their role more easily.

After all, the seller has had years to be familiar with the inner-workings of the business operations. You are just coming in for the first time and the staff are in a unique position to help you.

Give them some sort of framework to create the documentation. Whether this is recording screencasts, or writing out written procedures, get whatever you can in place.

Tools to help do this can be as simple as Quicktime for screenshots (or Jing for Windows computers), to services such as Way We Do, Zavanta, SystemHUB, Tightship, and Process Street.

Ask Each Employee About Their Desired Future Goals & Opportunities

A lot of buyers also like to use initial conversations with staff to discover what goals individual employees have with the company. Each employee may have a desire to work in a particular area and achieve certain ambitions.

After all, if they are already doing one job extremely well, who’s to say they are not capable of moving into a similar position within the company? This will empower them to make the transition period a success, and it would also signal the company’s enormous confidence in that person and their abilities. It’s only human nature to respond well to a compliment.

If jobs they would like to do are not immediately available, just listening to their desires, taking notes, and showing serious consideration can make a fantastic first impression. You could say (only if it is true obviously) that if the position eventually opens up once you are comfortable in your new role as company owner, then you would be extremely open to letting them try out for the role. This gives the employee a good reason not to quickly give up and leave for a new company.

One final advantage to going this route is that listening to employee’s requests for future company responsibilities may make you see business expansion possibilities you never knew existed. Remember, the staff is your most valuable resource! As such, crowdsource their skills and wisdom.

Consider Crafting Your Offer to Incentivize Staff to Stick Around

Many sellers, before finally selling to a new owner, do have many concerns for their employees, and a lot go above and beyond what they may typically be expected to do. They don’t run for the door, and never look back. Many go out of their way to listen to staff concerns, try to allay those fears, and perhaps even reward them for their loyalty.

After the sale of the company has gone through, some sellers will pay a bonus out of the sale money to their staff, especially the key staff, such as managers. It’s a nice way for the seller to say thank you, and it can also be used as a great way to encourage them to stay for at least the transition period.

It is not your place though as the buyer to request the seller pays a bonus to their staff. What the seller chooses to do with the sale money is entirely up to them. If they are not going to do it themselves, you may decide to take the opportunity to create a really good impression with the staff by paying the bonus yourself out of the money you were planning to pay the seller.

If you decide to go down this road though, make sure you put it down in black-and-white in the Letter of Intent. This way, there will be no misunderstandings later that could lead to the deal being damaged.

Ask The Seller To Help With The Staff Transition

This might seem like a natural thing for a seller to do, but you should always ask the seller to help you with the transition of the staff. Perhaps it hasn’t occurred to the seller to do this?

Have the seller introduce you, and ask them to manage those relationships initially. They know the staff better than you will initially, and anxious employees are more likely to go to who they know, rather than who they don’t know.

Ask For Documentation Of Procedures

This is probably one of the most important pieces of advice, regarding this subject – get as many procedures documented as possible.

We’ve already mentioned asking the employees to document their workflows, but also ask the business owner. There will be many duties the owner does by themselves which should also be put down in black and white. This will make your learning curve as shallow as possible.

Conclusion

Some buyers see staff as a nuisance, who are likely to gum up the works. But in reality the staff are the jewel of any business. Staff can make a business expand and grow, and it is the staff which the buying public may warm to, instead of yet another faceless online business.

So treat the staff with respect and courtesy, and include them in your transition plans. It will more than pay off in the end.